- How to Determine Overhead A Guide for Professional Services

- The True Cost of Doing Business and Why Overhead Matters

- Direct vs. Indirect Costs: The Core Distinction

- Direct Costs vs Indirect Costs At a Glance

- Identifying and Pooling Your Indirect Costs

- Uncovering Every Indirect Expense

- Creating Logical Cost Pools

- Calculating Your Firm’s Overhead Rate

- The Direct Labor Cost Method

- Example: A Small Engineering Firm

- Other Overhead Calculation Methods

- Comparing Overhead Rate Calculation Methods

- A More Advanced Approach: Activity-Based Costing (ABC)

- Applying Overhead to Projects and Client Rates

- From Project Costing to Client Pricing

- Calculating the True Total Project Cost

- Reverse-Engineering for a Fully-Loaded Hourly Rate

- Continuously Tracking and Monitoring Overhead

- Why Your Overhead Rate Is a Living Number

- Setting Up Systems for Success

- Using Reports to Spot Trends and Protect Profitability

- Common Questions About Determining Overhead

- How Often Should I Recalculate My Overhead Rate?

- What Are the Most Common Mistakes to Avoid?

- Can My Overhead Rate Be Too High or Too Low?

How to Determine Overhead A Guide for Professional Services

Figuring out how to determine overhead starts with separating costs into two buckets: money spent directly making something for a client (direct costs) and all the other essential expenses needed to run your business (indirect costs). Your overhead is the total of all those indirect costs. You’ll use this total to calculate a rate that ensures every single project covers its fair share of the business’s operational expenses.

The True Cost of Doing Business and Why Overhead Matters

Let’s be honest, calculating overhead can feel like a chore. It’s often seen as that tedious administrative task you just have to get through, rather than a strategic part of running your firm. But thinking of it as just “the cost of keeping the lights on” completely misses the bigger picture.

In reality, your overhead is the engine that powers your entire professional services firm. It’s the rent for your office space, the salaries for your indispensable administrative team, the software licenses your designers can’t work without, and the marketing that brings in new clients.

Without these investments, your billable work simply couldn’t happen.

Understanding this is the first real step toward transforming overhead from a necessary evil into a genuine strategic advantage for your firm.

Direct vs. Indirect Costs: The Core Distinction

To get your overhead right, you have to get this part right first. This separation is the foundation of accurate financial management and profitable project pricing.

-

Direct Costs: These are expenses you can tie directly to a specific client project. Think of the hours a consultant spends on a client engagement or the specific materials purchased for an architectural model. If you can assign a cost to a particular project code or client name, it’s a direct cost. For example, if your marketing agency hires a freelance photographer for a specific client’s ad campaign, that photographer’s fee is a direct cost.

-

Indirect Costs (Overhead): This is everything else. These are all the other expenses required to operate your business. They support all your projects but aren’t attributable to any single one. This includes everything from your accounting software subscription and your professional liability insurance to the coffee in the breakroom. For instance, the monthly subscription for your team’s project management tool supports all projects, so it’s an indirect cost.

To make it even clearer, let’s break it down side-by-side.

Direct Costs vs Indirect Costs At a Glance

This table offers a quick comparison to help you differentiate between costs directly tied to client projects and the indirect costs that make up your overhead.

| Cost Type | Definition | Examples for a Consulting Firm |

|---|---|---|

| Direct Costs | Expenses directly attributable to a specific project. | Billable hours of a senior consultant, specialized software purchased for a single client, travel expenses for a client site visit. |

| Indirect Costs (Overhead) | Expenses necessary for business operations but not tied to one project. | Office rent, administrative salaries, marketing budget, general software subscriptions (Drum, Xero), professional insurance. |

Thinking about your costs in these two distinct categories is non-negotiable for running a healthy services business.

The key takeaway is this: Every dollar you spend is either a direct cost fueling a specific project or an indirect cost fueling the entire business. Ignoring the latter is one of the fastest ways to underprice your services and bleed profit, even when you’re swamped with client work.

For a professional services firm, getting this right is crucial. Misclassifying an indirect cost as a direct one—or worse, forgetting to account for it at all—means you aren’t capturing the true cost of delivering your work. This leads to inaccurate project bids, misleading profitability reports, and ultimately, poor business decisions.

Mastering this distinction is your roadmap to building a more sustainable and financially sound firm.

Identifying and Pooling Your Indirect Costs

Alright, we’ve separated our direct and indirect costs. Now it’s time to get our hands dirty. Before you can even think about calculating overhead rates, you need a rock-solid, comprehensive list of every single indirect expense your firm has. This is the foundation of the whole process—get this wrong, and every calculation that follows will be off.

Think of it like this: if you miss a key ingredient in a recipe, the final dish is a bust. Same principle applies here. Overlook an indirect cost, and you’ll understate your overhead. That leads directly to underpricing your work and, you guessed it, tanking your profitability without even realizing it.

Your accounting software, like QuickBooks or Xero, is your best friend for this task. Don’t just skim the summary numbers. You need to run a detailed “Profit and Loss” or “Income Statement” report for the last 12 months. This gives you a complete baseline of what you’ve actually been spending.

Uncovering Every Indirect Expense

It’s easy to remember the big stuff like office rent. What often gets missed are the smaller, recurring costs that really add up over a year. You need to comb through your financial reports and hunt down every expense that isn’t directly tied to a client project.

Here are a few real-world examples you’ll likely find, broken down by firm type:

- For an Engineering Firm:

- Salaries: Time spent by project managers, admin staff, and your business development team that isn’t billable.

- Software: Those hefty annual licenses for CAD software, project management tools, and all your standard office apps.

- Insurance: Don’t forget Professional liability (Errors & Omissions) and general business insurance.

- For a Marketing Agency:

- Salaries: The slice of an account manager’s or strategist’s salary that goes to internal meetings, training, and sales pitches.

- Software: Monthly subscriptions to SEO tools (like Ahrefs or Semrush), social media schedulers, and your Adobe Creative Suite licenses.

- Marketing: This is a big one—your own firm’s advertising spend, any conference sponsorships, and the costs to create your own content.

- For an Architecture Practice:

- Facilities: Rent and utilities for your studio space are obvious, but what about cleaning services or minor repairs?

- Supplies: All the general office supplies, plotter paper, and printing costs that aren’t specifically billed back to a project.

- Professional Development: Dues for AIA or other professional groups, continuing education courses, and those all-important industry certifications.

The goal is to capture everything that supports your billable work without being a direct part of it. A forgotten software subscription or a miscategorized insurance payment can throw off your entire calculation. Precision here pays dividends later on.

Creating Logical Cost Pools

Once you have your complete list, the next move is to bring some order to the chaos. A long, messy list of expenses isn’t very useful for analysis. The solution is to group related expenses into logical categories called cost pools.

This isn’t just a pointless accounting exercise; it gives you incredible clarity on where your money is actually going. By pooling costs, you can instantly see if your facility expenses are creeping up or if you’re spending more on tech than you thought.

This is where proper time tracking and expense software can be a total game-changer, letting you tag expenses as they happen instead of sorting through a mess at the end of the year.

Here’s a simple way to structure your cost pools:

| Cost Pool Category | Typical Expenses Included |

|---|---|

| General & Administrative (G&A) | Non-billable salaries, office supplies, accounting fees, legal services, bank fees. |

| Facilities & Occupancy | Rent or mortgage, utilities (electricity, internet, water), property insurance, repairs, cleaning. |

| Technology & Software | All software subscriptions, IT support contracts, computer hardware depreciation, phone systems. |

| Business Development & Marketing | Advertising costs, sales staff salaries, conference fees, website hosting, marketing materials. |

By slotting every indirect cost into one of these pools, you transform that chaotic list into a structured, actionable financial map. This organization is the final prep step before you can confidently calculate an overhead rate that truly reflects the cost of running your business.

Calculating Your Firm’s Overhead Rate

Okay, you’ve done the hard work of gathering your indirect costs and sorting them into logical pools. Now for the main event: crunching the numbers to find your firm’s overhead rate.

This isn’t just an accounting exercise. This is the step that turns those raw expense figures into a powerful, practical metric you can use for pricing, budgeting, and, most importantly, protecting your profitability.

Don’t worry if you’re not a numbers person. The most common methods are surprisingly straightforward. Even a simple, consistently applied rate will give you a massive strategic advantage over firms that are just guessing. We’ll walk through a few key approaches, starting with the one most services firms rely on.

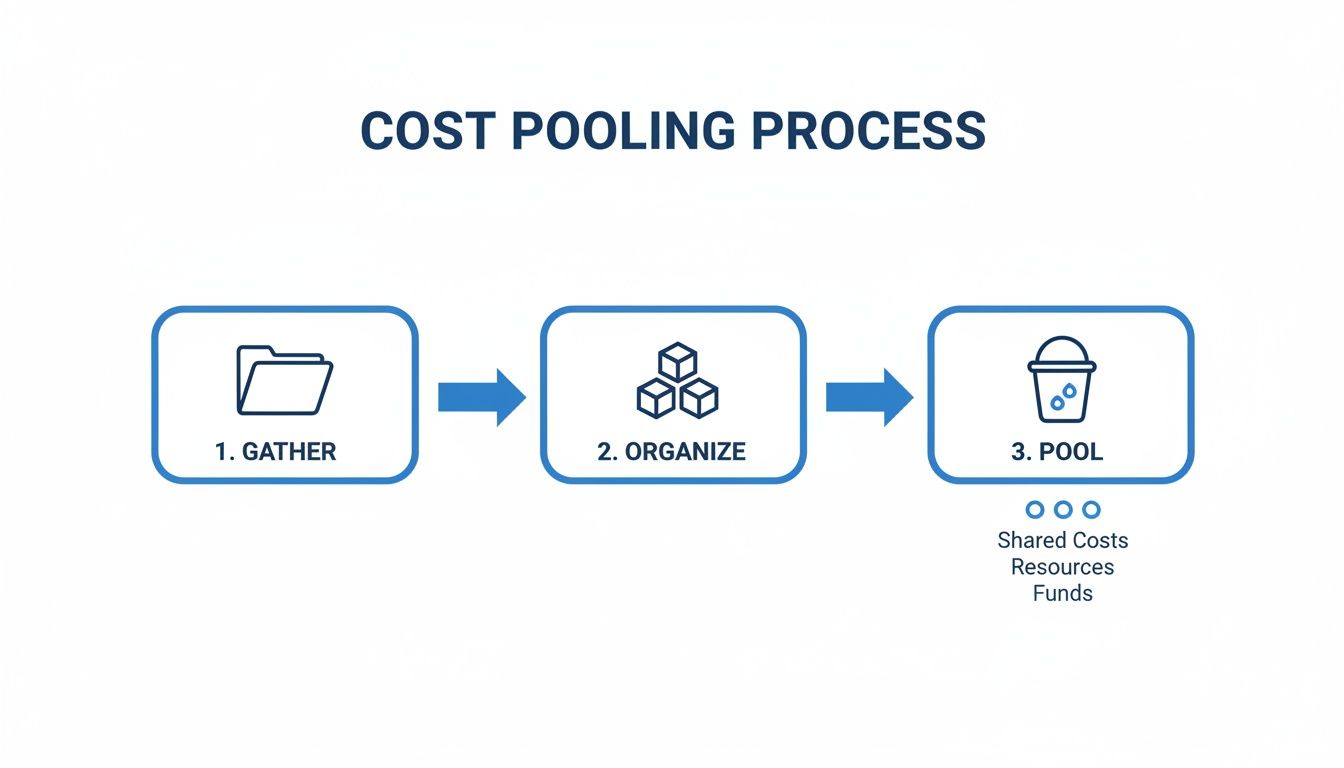

This visual shows the simple process of gathering your financial data, organizing it into logical groups, and pooling it together before you start your calculations.

This process ensures that when you move to the calculation phase, you’re working with a complete and organized picture of your firm’s indirect expenses.

The Direct Labor Cost Method

For most professional services firms—think engineering, marketing, and architecture—your biggest single expense is almost always your people. It just makes sense.

Because of this, the most common and often most effective way to calculate your overhead rate is as a percentage of your direct labor costs. It’s built on a simple, logical premise: the more billable hours a project requires, the more of the firm’s support resources it likely consumes.

The formula is clean and easy to apply:

Overhead Rate = (Total Indirect Costs / Total Direct Labor Costs) x 100

Let’s see this in action with a real-world scenario.

Example: A Small Engineering Firm

Imagine a small civil engineering firm with the following annual financials:

- Total Indirect Costs: $300,000 (this includes rent, admin salaries, software, etc.)

- Total Direct Labor Costs: $500,000 (this is the total cost of salaries for engineers working directly on client projects)

Plugging these numbers into our formula:

- ($300,000 / $500,000) x 100 = 60%

This firm’s overhead rate is 60%. This is a critical piece of business intelligence. It means for every dollar the firm spends on an engineer’s billable salary, it must add another 60 cents just to cover the operational costs of the business.

Knowing this number is the difference between profitable work and accidentally bidding on projects at a loss.

Other Overhead Calculation Methods

While the direct labor method is a fantastic starting point, it’s not a one-size-fits-all solution. Depending on your business model, other methods might give you a more accurate picture of your true costs. Let’s look at a couple of other popular approaches.

The table below breaks down the most common methods, helping you see at a glance which one might be the best fit for your firm’s unique situation.

Comparing Overhead Rate Calculation Methods

| Method | How It Works | Best For | Pros & Cons |

|---|---|---|---|

| Direct Labor Cost Method | (Total Indirect Costs / Total Direct Labor Costs) x 100 |

Service-based firms where labor is the primary driver of project costs (e.g., consulting, architecture, marketing agencies). | Pro: Simple, logical, and easy to calculate. Directly ties overhead to the primary cost driver. Con: Can be inaccurate if projects have significant non-labor direct costs (materials, subcontractors). |

| Direct Cost-Based Method | (Total Indirect Costs / Total *All* Direct Costs) x 100 |

Firms with significant non-labor direct costs, such as large material purchases, equipment rentals, or heavy subcontractor use. | Pro: Provides a more balanced allocation when projects have a mix of labor, materials, and other direct expenses. Con: Can be slightly more complex to track all direct costs consistently across projects. |

| Activity-Based Costing (ABC) | Divides overhead into multiple cost pools and allocates them based on specific activities (e.g., IT costs by employee count, facility costs by square footage). | Larger, more complex firms with diverse service lines that consume overhead resources differently. | Pro: Extremely accurate and provides deep insights into what truly drives costs. Con: Can be complex and time-consuming to set up and maintain. Often requires more sophisticated accounting practices. |

Choosing the right method is all about understanding what drives costs in your business. A simple method applied consistently is far better than a complex one that’s never used.

A More Advanced Approach: Activity-Based Costing (ABC)

For more complex firms with diverse service lines, a single, firm-wide overhead rate might not be precise enough. It can sometimes feel like a blunt instrument when you need a scalpel.

For instance, a design team using expensive rendering software might consume far more technology overhead than a strategy team that primarily needs standard office software. A single rate would unfairly burden the strategy team with costs they aren’t generating.

This is where Activity-Based Costing (ABC) offers a much more granular and accurate picture. Instead of one single cost pool and one rate, ABC uses multiple cost pools, each with its own “cost driver.” A cost driver is simply the activity that causes those costs to happen.

You might end up with something like this:

- Facility Costs driven by the square footage each department uses.

- IT Support Costs driven by the number of employees in each department.

- Software License Costs driven by the specific software seats used by each team.

By allocating overhead this way, you get a much truer understanding of your cost structure. This isn’t just a new idea; it’s a proven strategy for gaining clarity. The practice of determining overhead in consulting firms has historically leaned on direct labor, but as technology plays a bigger role, that can distort the true costs.

Think about it: after a manufacturing plant replaced 90% of its workforce with robots, allocating overhead based on the few remaining labor hours would be completely misleading. Recognizing this, Chrysler adopted Activity-Based Costing back in 1991 and reported savings 10 to 20 times the implementation cost, all by gaining a clearer picture of its cost drivers.

While a full-blown ABC implementation can be intensive, even adopting a simplified version can provide invaluable insights for a growing firm. The key is to choose the method that best reflects your firm’s unique operational reality.

Applying Overhead to Projects and Client Rates

You’ve done the heavy lifting—you’ve tracked down all your indirect costs and calculated your firm’s overhead rate. Now for the most important part: putting that number to work. This is where a simple metric on a spreadsheet transforms into a powerful tool that drives strategic pricing and protects your profitability.

This is the bridge between knowing your costs and ensuring every single project you take on is financially sound. Applying your overhead rate correctly builds a crucial buffer against underbidding, which is one of the fastest ways professional services firms lose money without even realizing it.

From Project Costing to Client Pricing

Let’s walk through a complete, real-world example to see how this all comes together. We’ll stick with our friendly engineering firm from the last section, which we determined has a 60% overhead rate.

Imagine this firm is bidding on a new structural analysis project. The first thing they do is estimate the direct costs—the hands-on labor and materials needed to get the job done.

- Estimated Direct Labor: The project will need 200 hours from a senior engineer whose all-in cost (salary, benefits, taxes) is $75/hour. So, 200 hours x $75/hour = $15,000.

- Other Direct Costs: They anticipate needing specialized software rentals and plotter printing services specific to this job, totaling $1,000.

- Total Direct Costs: $15,000 + $1,000 = $16,000.

This is where so many firms go wrong. They stop here, slap on a profit margin, and send the quote. It’s a critical mistake. To find the true cost of delivering this project, they have to apply their overhead rate.

Calculating the True Total Project Cost

That overhead rate accounts for this project’s fair share of everything else that keeps the lights on—the office rent, the admin salaries, the marketing budget, you name it.

- Calculate the Overhead to Apply:

Overhead Cost = Direct Labor Cost x Overhead Rate$15,000 x 60% (0.60) = $9,000

- Determine the True Total Cost:

True Cost = Total Direct Costs + Overhead Cost$16,000 + $9,000 = $25,000

This $25,000 figure is the firm’s actual breakeven point. It’s the rock-bottom price they must charge just to cover their expenses for this specific project.

Understanding your true total cost is non-negotiable. It’s the baseline below which you are actively paying to do the work. Any price below this number is a loss, regardless of how busy it makes your team feel.

With the true cost established, the firm can finally add a healthy profit margin to get to their final client price. If they’re aiming for a 20% profit margin:

- Profit Amount:

$25,000 x 20% (0.20) = $5,000 - Final Client Price:

$25,000 + $5,000 = $30,000

By following this simple process, the firm can bid with total confidence, knowing their price covers every cost and delivers the planned profit. For more strategies on this, check out our guide on how to price consulting services.

Reverse-Engineering for a Fully-Loaded Hourly Rate

The same logic is absolutely essential for setting profitable hourly billing rates for your team members. A fully-loaded hourly rate is a billable rate that covers not just an employee’s salary and benefits, but also their slice of the firm’s overhead and a built-in profit margin.

Let’s calculate one for that senior engineer from our example.

- Employee’s Hourly Cost: We already know this is $75/hour.

- Overhead Coverage Per Hour: To cover their share of overhead, we apply the 60% rate directly to their cost:

$75 x 60% = $45/hour. - Breakeven Rate: This is the employee’s direct cost plus their overhead portion:

$75 + $45 = $120/hour.

That $120/hour is the firm’s breakeven rate for this specific employee. Any billable hour charged below this means the firm is losing money on their time.

Finally, we bake in the desired 20% profit margin:

- Profit Per Hour:

$120 x 20% = $24/hour - Fully-Loaded Billable Rate:

$120 + $24 = $144/hour

To stay profitable, the firm needs to bill this engineer out at a minimum of $144/hour. It’s that straightforward.

This direct-cost-based allocation is a powerful and common method for service firms. It works by distributing indirect expenses proportionally to each project’s direct costs, operating on the simple assumption that bigger, more labor-intensive projects naturally consume more overhead resources. It just makes sense.

Continuously Tracking and Monitoring Overhead

Calculating your firm’s overhead rate is a huge step forward, but it’s not the finish line. Think of that initial calculation as a snapshot—a single picture taken at one moment in time. To truly master your firm’s financial health, you need to turn that snapshot into a motion picture, continuously tracking how your costs evolve.

A static overhead rate becomes less accurate with every new hire, every new software subscription, and every change in your business. What was a precise measure of your costs six months ago could be dangerously misleading today, causing you to underprice major projects without even realizing it.

Why Your Overhead Rate Is a Living Number

Your business is dynamic, and your overhead rate must be too. Relying on an outdated number is like navigating with an old map; it doesn’t account for the new roads and obstacles that have appeared along the way. Several common business changes can torpedo the accuracy of your indirect cost calculations.

It’s critical to review and potentially recalculate your rate at least quarterly or semi-annually, and immediately following any major operational shift.

Key triggers that demand a review include:

- Hiring New Staff: Adding non-billable team members, like an administrative assistant or a marketing coordinator, directly increases your overhead.

- Moving Offices or Renewing a Lease: A change in rent is often one of the largest shifts in a firm’s fixed indirect costs.

- Investing in New Technology: A major software rollout or hardware upgrade can add substantial new expenses to your tech cost pool.

- Significant Salary Adjustments: Annual raises or market adjustments for your non-billable team will push your overhead costs higher.

Treating your overhead rate as a living metric is the only way to ensure your pricing and profitability analysis remain grounded in reality.

Setting Up Systems for Success

The key to effective monitoring is building good habits into your daily operations from day one. This means not waiting until the end of the quarter to sort through a mountain of uncategorized expenses. Proactive tracking makes regular reviews simple rather than stressful.

Start with your time and expense tracking. It’s essential to create clear categories that distinguish between different types of work. Every hour your team logs should fall into a specific bucket.

- Billable Project Work: Time spent directly on client deliverables.

- Non-Billable Administration: Time spent on internal meetings, paperwork, and general operations.

- Business Development: Time spent on sales calls, proposal writing, and networking.

This level of detail gives you a crystal-clear view of how your most valuable resource—your team’s time—is being allocated. By integrating this with smart expense management, where every receipt is tagged to a cost pool as it comes in, you create a real-time feed of your firm’s financial activity. For more insights, you can learn about linking project management and accounting systems.

Using Reports to Spot Trends and Protect Profitability

With clean, real-time data, you can move from reactive adjustments to proactive, data-driven decisions. Your goal is to spot negative trends before they become serious problems. One of the most important metrics to watch is overhead as a percentage of total revenue. If this number starts creeping up, it’s an early warning sign that your indirect costs are growing faster than your income.

Staying ahead of cost creep is a constant discipline. Waiting for the annual P&L to tell you that your overhead has ballooned is too late—the damage to your project profitability has already been done. Real-time reports give you the power to act immediately.

More advanced methods like Activity-Based Costing (ABC) can provide even deeper insights by using multiple activity drivers instead of a single rate, which is particularly effective in complex consulting environments. Traditional methods based solely on direct labor can become less accurate as firms automate. Chrysler’s famous shift to ABC in 1991, for example, generated returns of 10-20 times the investment at some sites by pinpointing and cutting inefficiencies that a single-rate system would have missed.

Regardless of the method, regularly updating your rates is crucial for making informed decisions based on current data. By establishing a regular rhythm of review and leveraging real-time reporting, you turn overhead management from a periodic chore into a continuous strategic advantage that safeguards your firm’s financial future.

Common Questions About Determining Overhead

After you’ve walked through the process of identifying, calculating, and applying your overhead, a few practical questions almost always pop up. This is where the theory hits the road. Think of this next part as a quick-reference guide for the most common sticking points we see firms run into when they start actively managing these costs.

How Often Should I Recalculate My Overhead Rate?

Your overhead rate is not a “set it and forget it” number. Your business is a living, breathing thing, and your rate needs to reflect that reality. Relying on a rate from two years ago is like trying to navigate a new city with an old map—it will absolutely lead you astray.

As a general rule, you should plan to review and recalculate your overhead rate at least semi-annually. If your business is in a high-growth phase, you’ll want to bump that up to quarterly.

However, you should immediately recalculate it after any significant business event.

Key triggers for an immediate recalculation include:

- A major change in staffing: Hiring several new employees, especially non-billable staff, will directly inflate your indirect salary costs.

- Moving to a new office: A jump in rent is one of the biggest drivers of overhead and requires an immediate update.

- Significant technology investments: Rolling out new firm-wide software or upgrading hardware will alter your technology cost pool and needs to be factored in right away.

What Are the Most Common Mistakes to Avoid?

Learning how to determine overhead is a process, and a few common pitfalls can trip up even the most diligent managers. Just being aware of them is the best way to keep your calculations accurate and genuinely useful.

The most frequent mistake we see is simply forgetting certain indirect costs. It’s easy to remember big-ticket items like rent, but smaller recurring expenses can add up fast. Things like bank fees, professional membership dues, and specific software subscriptions can amount to a significant number over a year. Your best defense here is a thorough review of your annual profit and loss statement.

Another major error is using outdated data. Calculating your rate based on last month’s numbers when you just hired three new people will give you a misleadingly low figure. You should always use the most current data you have, typically a trailing 12-month period, but make sure to adjust it for any recent, major changes.

The goal is to create a rate that reflects your business as it operates today, not as it did last year. An inaccurate rate, whether too high or too low, leads to flawed pricing decisions and erodes profitability.

Can My Overhead Rate Be Too High or Too Low?

Yes, and both scenarios tell an important story about your business. Your overhead rate isn’t just a number; it’s a key performance indicator that offers powerful insights into your firm’s operational efficiency and pricing strategy.

A very high overhead rate might indicate a few things. It could mean your firm is inefficient, with too much non-billable time or bloated administrative expenses relative to your direct labor. On the other hand, it could be a strategic investment in growth, like a major marketing push or a new internal R&D team. For example, a marketing agency investing heavily in new video equipment might see a temporary spike in its overhead rate, which is perfectly fine if it leads to higher-value client work down the road.

Conversely, a very low overhead rate might seem like a good thing, but it can also be a red flag. It could signal that you’re underinvesting in critical support functions like marketing, technology, or professional development, which could hamstring your firm’s long-term growth and competitiveness. If your tech firm’s overhead is low because you’re still using outdated computers that constantly crash, that “efficiency” is actually costing you money in lost productivity.

Understanding what your overhead rate is telling you allows you to make informed, strategic adjustments to protect your firm’s financial health.

Ready to stop guessing and start making data-driven decisions about your firm's profitability?

Drum unifies your projects, time tracking, and financials into a single source of truth, giving you the real-time insights you need to determine overhead accurately and price your work with confidence..

Start your free 14-day trial and discover a better way to run your studio.